The Ultimate Guide To Kam Financial & Realty, Inc.

The Ultimate Guide To Kam Financial & Realty, Inc.

Blog Article

Getting My Kam Financial & Realty, Inc. To Work

Table of ContentsExcitement About Kam Financial & Realty, Inc.Kam Financial & Realty, Inc. Can Be Fun For EveryoneKam Financial & Realty, Inc. - An OverviewSome Known Facts About Kam Financial & Realty, Inc..Some Ideas on Kam Financial & Realty, Inc. You Should KnowLittle Known Facts About Kam Financial & Realty, Inc..The Ultimate Guide To Kam Financial & Realty, Inc.

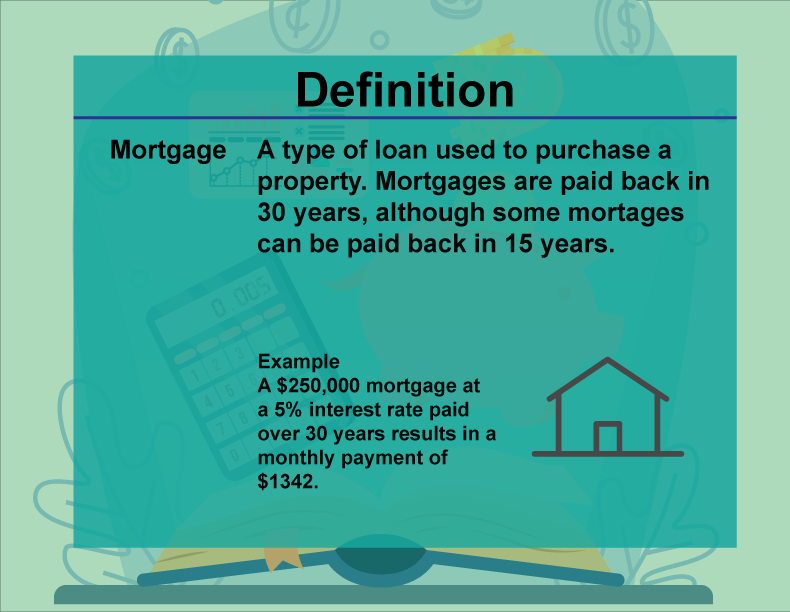

Purchasing a home is a significant landmark in lots of people's lives. However, that doesn't indicate the procedure is clear to those individuals. The home acquiring procedure entails numerous actions and variables, implying each person's experience will certainly be one-of-a-kind to their family members, monetary situation, and desired property. Yet that doesn't suggest we can't help make feeling of the mortgage process.A is a kind of funding you utilize to get residential or commercial property, such as a home. A financial organization or "lending institution" will offer you cash and they will certainly require you to utilize the home as security. This is called a secured car loan. Usually, a lender will give you a collection quantity of money based upon the worth of the home you wish to purchase or possess.

The Ultimate Guide To Kam Financial & Realty, Inc.

To get a mortgage, you will require to be a minimum of 18 years old. Aspects that aid in the mortgage procedure are a dependable income resource, a strong credit history, and a moderate debt-to-income ratio. (https://yoomark.com/content/kam-financial-realty-inc-our-mission-serve-our-customers-honesty-integrity-and-competence). You'll find out more concerning these factors in Component 2: A is when the home owner obtains a new home loan to change the one they presently have in location

A features similarly to a very first home mortgage. A runs a bit differently from a typical mortgage lending and is comparable to a credit history card.

This co-signer will certainly concur to pay on the mortgage if the consumer does not pay as agreed. Title business play a vital function ensuring the smooth transfer of home possession. They look into state and area records to verify the "title", or possession of your home being purchased, is complimentary and free from any kind of various other home loans or responsibilities.

How Kam Financial & Realty, Inc. can Save You Time, Stress, and Money.

In addition, they offer written guarantee to the loaning establishment and develop all the documentation needed for the mortgage. A down repayment is the amount of money you need to pay in advance towards the purchase of your home. If you are buying a home for $100,000 the lending institution might ask you for a down repayment of 5%, which suggests you would be required to have $5,000 in cash money as the down settlement to purchase the home. (https://urlscan.io/result/955ff859-6761-409a-8342-610d6278222a/).

The principal is the amount of money you receive from the lending institution to acquire the home. In the above example, $95,000 would certainly be the amount of principal. A lot of lenders have traditional home mortgage guidelines that permit you to borrow a specific percent of the value of the home. The portion of principal you can borrow will vary based upon the mortgage program you get approved for.

There are special programs for novice home customers, veterans, and low-income customers that permit reduced deposits and higher percentages of principal. A home mortgage lender can assess these alternatives with you to see if you qualify at the time of application. Interest is what the loan provider fees you to obtain the cash to acquire the home.

More About Kam Financial & Realty, Inc.

If you were to get a 30-year (360 months) home loan and borrow that same $95,000 from the above instance, the overall amount of interest you would certainly pay, if you made all 360 month-to-month repayments, would be a little over $32,000. Your monthly settlement for this financing would certainly be $632.

When you have a home or residential property you will have to pay residential or commercial property tax obligations to the region where the home lies. Most lending institutions will require you to pay your tax obligations with your home loan payment. Real estate tax on a $100,000 car loan can be about $1,000 a year. The lender will certainly split the $1,000 by 12 months and include it to your payment.

See This Report about Kam Financial & Realty, Inc.

Once again, due to the fact that the home is viewed as collateral by the lending institution, they wish to ensure it's shielded. House owners will certainly be needed to provide a copy of the insurance coverage to the lender. The annual insurance coverage plan for a $100,000 home will certainly cost approximately $1,200 a year. Like taxes, the lender will likewise offeror sometimes requireyou to include your insurance coverage costs in your month-to-month payment.

Your repayment now would certainly boost by $100 to a brand-new total of $815.33$600 in concept, $32 in rate of interest, $83.33 in taxes, and $100 in insurance policy. The lending institution holds this cash in the exact same escrow account as your real estate tax and makes settlements to the insurer on your part. Closing costs describe the costs connected with refining your car loan.

Kam Financial & Realty, Inc. Can Be Fun For Anyone

:max_bytes(150000):strip_icc()/dotdash-TheBalance-calculate-mortgage-315668-final-fd8c0ed392cd40118439cd1c23317e99.jpg)

This ensures you comprehend the complete price and consent to proceed before the finance is funded. There are various programs and lending institutions you can pick from when you're purchasing a home and getting a home loan who additional resources can aid you browse what programs or choices will certainly function best for you.

The Ultimate Guide To Kam Financial & Realty, Inc.

Lots of banks and property agents can help you understand just how much cash you can invest on a home and what funding amount you will receive. Do some research, but additionally request for recommendations from your good friends and household. Discovering the right partners that are an excellent fit for you can make all the difference.

Report this page